Outlook

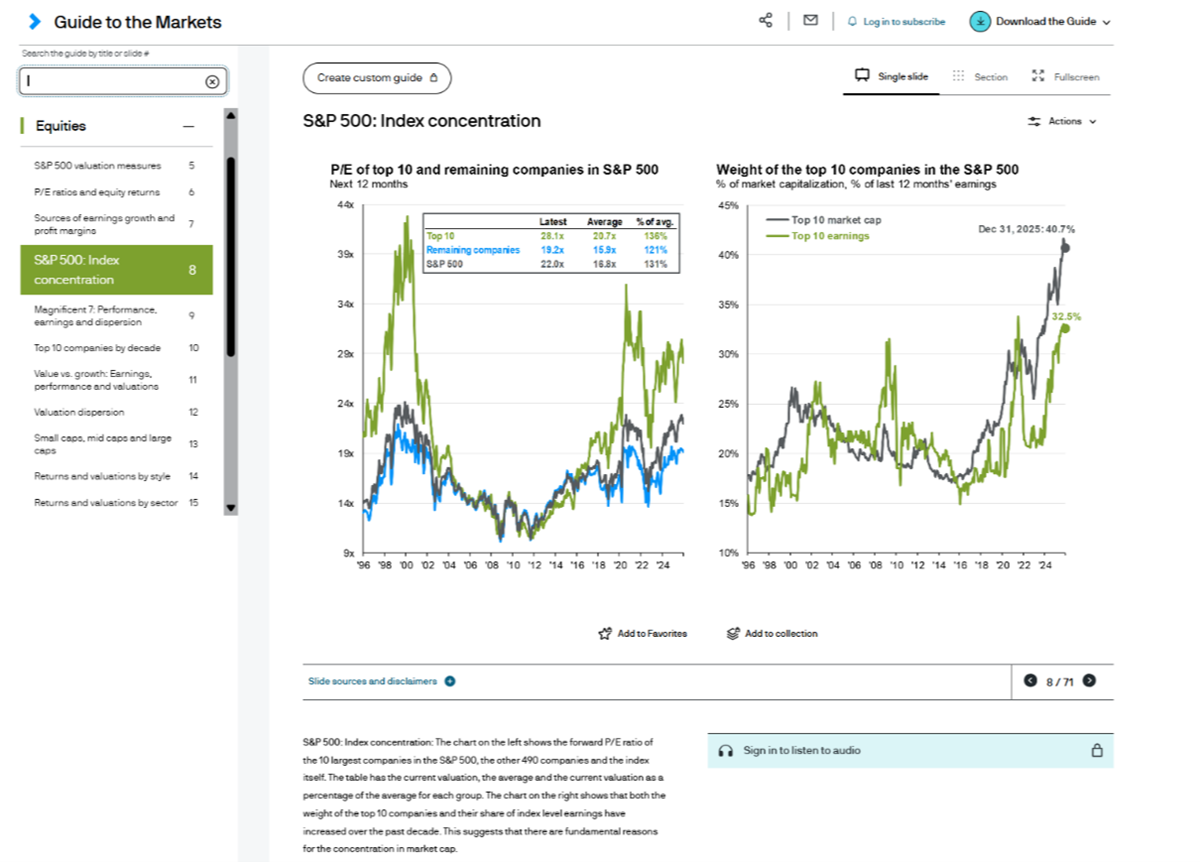

By the end of 2025, the 10 largest companies in the S&P 500 Index represented 41% of its total size in terms of market capitalization (price times total shares outstanding for each company) - slightly below all-time-high levels reached earlier in late-2025.1 Further, the earnings for these 10 companies reached a historically high 33% (slightly less than its all-time high in 2021). This is all to say that in 2025, the largest companies in the Index were historically large in terms of market valuation and the sheer dollar amount of profits these businesses earned. While this does not present any conclusive forecast about what 2026 will bring for the largest companies in the S&P 500, historic peaks suggest caution - at least as it relates to market capitalization peaks, which occurred in the 2000, 2008, and 2021 time-frames which coincided with bear markets. On the other hand, when the largest companies simply earned a lot of profits, specifically periods of peak profits relative to the overall S&P 500, subsequent index returns results were generally better --- such as the 2002-2003 time frame when profits peaked and the recovery from the dot-com bust gathered steam. As a result, today's situation is a bit uncertain for the largest companies. However, the excess valuation peak vs. profits (41% vs. 33%) may imply that some caution is worthwhile. Either way, we find 2026 as a good time to consider rebalancing out of overweight positions residing in the top 10 spots of the index.

. . .

U.S. equities ended last week navigating a mix of geopolitical tensions, policy headlines, economic data releases, and early-season corporate earnings, yet markets continued to demonstrate notable resilience.

CPI Data: Inflation Trends and Market Implications The latest CPI report showed inflation broadly aligned with expectations. Headline CPI rose 0.3% in December and 2.7% year over year, while core CPI increased 0.2% on the month and 2.6% annually, coming in slightly cooler than forecast.2 This affirmed the ongoing narrative of gradual disinflation, even as inflation remains above the Federal Reserve’s 2.0% long run target. Markets interpreted the data as consistent with a continued easing in price pressures, but not decisive enough to meaningfully alter near term monetary policy expectations. The futures market maintained the view that the Federal Reserve is likely to keep rates on hold at its upcoming meeting, with any potential rate cuts likely deferred until mid year.3 Overall, the path back toward the Fed’s inflation target is expected to remain uneven, and policymakers will likely require sustained evidence of cooling before shifting their stance.

Corporate Earnings: Financials Major U.S. banks delivered generally solid fourth-quarter results, supported by resilient loan growth, improved net interest income, and stable credit quality across consumer businesses.4 Banks benefited from a meaningful rebound in investment banking activity, with dealmaking and capital markets revenues strengthening, while trading desks saw heightened activity amid persistent market volatility. Despite overall healthy results, bank stocks slipped as executives highlighted potential headwinds—including the administration’s proposed 10% one year cap on credit card interest rates, which banks warned could pressure lending economics. Even so, the broader earnings landscape remained supportive. Expectations for continued corporate spending, along with healthy operating fundamentals, helped reinforce confidence in long term equity positioning. Overall, while geopolitical and policy uncertainties will likely continue to generate noise, the market's muted reaction suggests that investors currently view these risks as secondary to the more durable economic and corporate trends (moderating inflation, steady earnings momentum, and a resilient economy) that remain broadly encouraging heading into the next phase of 2026.

[1] https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/ [2] Consumer Price Index - December 2025 [3] FedWatch - CME Group [4] Bank Earnings Surge as Wall Street Bets on a Broad Earnings Rally - Barron's

|