Outlook Volatility in both the stock and bond markets, as measured respectively by the VIX index1 and MOVE index2, which are currently demonstrating that investors are not excessively worried about the investment climate. And why should they be? So far this quarter, 83% of companies in the S&P 500 have reported a positive earnings surprise, and 79% have reported a positive revenue surprise.3 Further, real-time economic growth is estimated to be a decent 3.9% according to the Atlanta Federal Reserve Bank.4 Aside from generally good news on the economy and earnings front, the largest technology companies have updated investors on their spending plans - and it is quite robust. While this is generally positive for the tech sector, overinvestment may also be a sign of a heightened risk environment in the years ahead.5 From our perspective, 2025 remains a good time for finding and investing in high-quality businesses at reasonable prices. While we plan on keeping a close eye on growing risks, we believe investors can keep risks in check by maintaining reasonable expectations and remaining diligent.

. . .

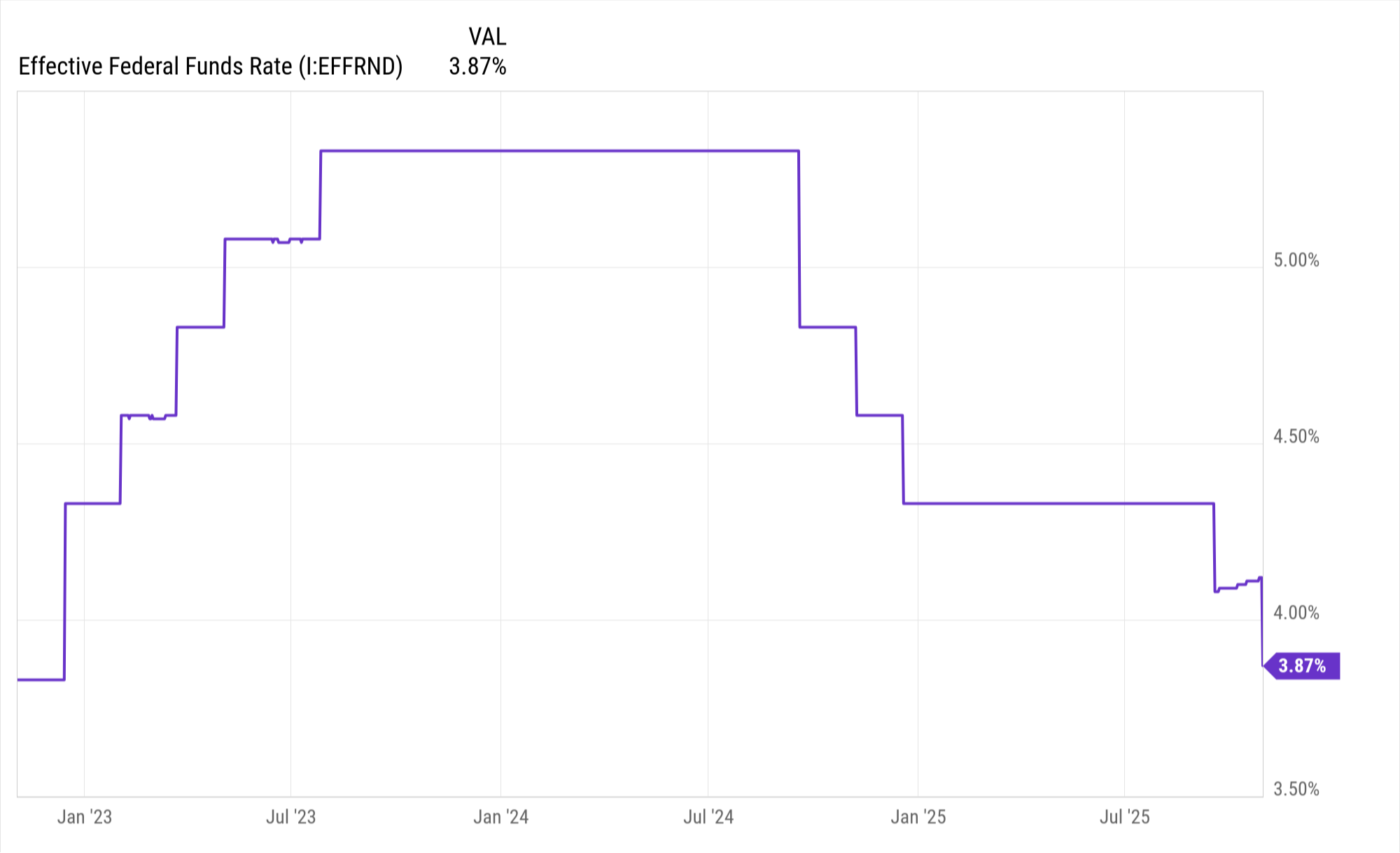

The markets continue to make impressive gains amid a turbulent October, closing out the third consecutive week of positive returns and the sixth straight month of gains. Sentiment this week was boosted by big tech earnings, positive trade talks between the U.S. and China, and a 25bps (0.25%) rate cut from the central bank. Albeit commentary from Fed Chairman Jerome Powell damped the mood as he turned more hawkish, warning investors that a December cut is “far from” a foregone conclusion. Powell indicated it may “make sense to be more cautious” as the Fed monitors slowing labor-market dynamics. So, while the pace at which rate cuts will occur is uncertain, it does appear that rates are heading lower.

As for the October meeting, the central bank lowered its overnight lending rate to a target range of 3.75 – 4.00% and announced to end the reduction of U.S. government bond holdings on the balance sheet effective December 1st. The Fed bought large quantities of bonds from investors, following the pandemic, to help lower longer-term interest rates and promote growth. Recently, the central bank has been slowly letting the bonds roll off the balance sheet. The committee now considers the current level of assets on the balance sheet to be back in the normal range. Both announcements were widely anticipated. As for corporate earnings, roughly two-thirds of S&P 500 companies have reported, with a majority delivering stronger than expected top-line (revenue) and bottom-line (profits) despite recent headwinds (i.e., higher tariffs).3

Specifically, this week, five of the Magnificent Seven companies reported. Overall, the mega-cap tech companies proved that growth and profitability remain resilient, boosted by AI monetization across cloud platforms and semiconductors. Guidance pointed to strong potential growth, while elevated spending (capital expenditures) guidance related to AI infrastructure investments sparked concern among investors. Lastly, turning to politics, a highly anticipated meeting between President Trump and China’s President Xi resulted in easing trade tensions between the two countries. Trump has agreed to lower tariffs related to fentanyl from 20% to 10%, which would bring the effective tariff rate on Chinese imports to 47% from 57%. In exchange, China has agreed to a one-year pause of new restrictions on exports of critical rare earth minerals and will start buying soybeans from American farmers again. 6

[1] https://www.google.com/search?q=vix+index [2] https://www.google.com/search?q=move+index [3] https://investor.factset.com/financials/quarterly-results [4] https://www.atlantafed.org/cqer/research/gdpnow [5] https://www.morningstar.com/markets/why-ai-spending-spree-could-spell-trouble-investors [6] Xi-Trump meeting sparks optimism in China — but many wonder what comes next |