Outlook As we head towards year-end, what seems to be the most important economic story of 2025 is the collision between aggressive new trade tariffs and the massive acceleration of Artificial Intelligence (AI) investment. Tariff-related revenues jumped from $97 billion in the 1st quarter to over $267 billion three months later.1 Despite the warnings from many economists, inflation has not been the defining consequence of tariffs. This story is not over but may not be the purported trainwreck that many feared - we shall see. While importers have been wringing their hands over tariff duties, tech companies have been transitioning from a phase of Artificial Intelligence (AI) experimentation to massive infrastructure build-out. The "Hyperscalers"—Amazon, Microsoft, Alphabet (Google), and Meta— accounted for the lion's share of investment (approximately $400 billion in 2025,2 with the goal of building the physical backbone for AI. In 2026, we will be looking for signs of excess in this space as funding for AI projects shifts from the use of existing funds (i.e., from earnings) to raising new capital (i.e., debt). Add in the longest government shutdown in U.S. history and significant market volatility, and the defining theme for 2025 has been how the economy managed to remain resilient despite these strong economic currents. We remain constructive on continued U.S. economic growth for 2026 and will continue to keep our eye on these developing stories in addition to many other important data points, such as those related to employment and earnings.

. . .

As 2025 draws to a close, investors receive some of the final economic data metrics for the year, with the delayed U.S. employment and inflation reports coming to light in the prior week.

Cooling Inflation

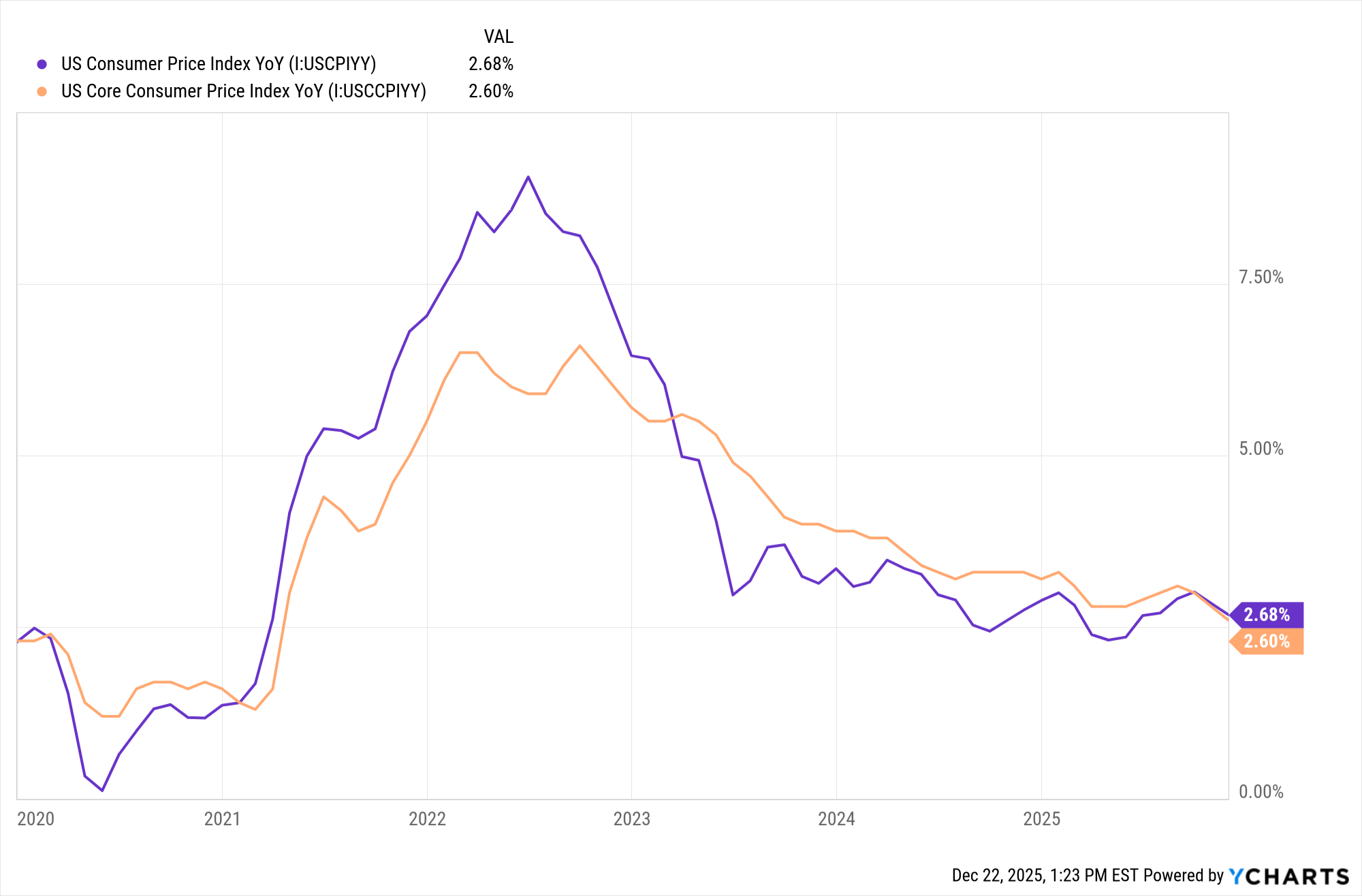

November’s inflation data showed a big surprise, as consumer prices rose far less than expected. The consumer price index (CPI)showed the annualized headline figure slowed to 2.7% last month from 3.1%. While the core CPI, which excludes volatile food and energy prices, also cooled more than expected, easing to 2.6% from 3.0%. The monthly increases also came in less than expected, rising just 0.2% for both measures, compared to estimates of 0.3%. This data is warranted at least slight uncertainty, due to complications from the government shutdown disrupting the data collection process. The shutdown led to the cancellation of the October CPI release. The Bureau of Labor Statistics (BLS) was unable to retroactively collect a portion of the October prices; however, used some “nonsurvey data sources” to make the index calculations. Therefore, it is possible the distortions seen in November’s report may overstate the true extent of deceleration in inflation. An additional month or two of releases may be needed to gain a clearer understanding of the trend in inflation, specifically of key underlying factors such as price movements in shelter, energy, food, or more generally goods and services. Market consensus indicates inflation may remain rangebound in the beginning months of 2026, above the Fed’s 2% target, whilst showing improvements from 2025. Shelter costs remain a large portion of inflation, and ongoing moderate decreases in housing are expected to encourage softening in services inflation.

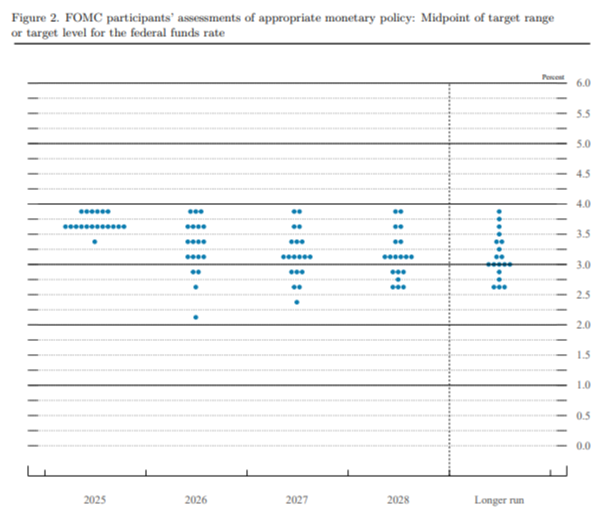

Low Hiring/Low Firing Labor Market The November non-farm payrolls reportshowed mixed results. Similar to the CPI report, the BLS released the delayed October and November employment figures. The U.S. economy added 64,000 jobs in November (more than expected), after posting a 105,000 decline in October. The payroll drop in October was widely anticipated after a surprise increase of 108,000 in September, along with influences from the shutdown. Much of the October decline stemmed from a steep fall in government employment as deferred layoffs instituted earlier this year took effect. Jobs added remain concentrated in healthcare, while transportation and warehousing recorded job losses.October’s unemployment rate was unable to be calculated by the BLS during the shutdown, but the November release showed the unemployment rate rose to a new cycle high of 4.6%. The 0.1% rise in the unemployment rate was largely attributed to the increase in the labor force. The labor force participation rate edged higher to 62.5%. The job climate continues to display a low-hiring, low-firing state. December’s numbers (January’s release) for employment and inflation are expected to hold more weight, due to increased clarity in the data. Fed Chairman Powell cautioned against over-interpreting November’s figures, given the disruptions in data collection. Overall, the markets are encouraging of the solid economy with participants still expecting a hold at the January policy meeting, while slightly increasing expectations of a cut in March.3

[1] https://fred.stlouisfed.org/series/B235RC1Q027SBEA [2] https://www.statista.com/chart/35046/capital-expenditure-of-meta-alphabet-amazon-and-microsoft/ [3] FedWatch - CME Group

|