Outlook The Federal Reserve Bank of Atlanta’s latest GDPNow model1 estimate for 4th quarter of 2025 surged to a striking 5.4%, a significant divergence from the Blue Chip consensus, which remains anchored near 1.0%. The model's estimate nearly doubled in early January, vaulting from 2.7% to the current high following the January 8 release of international trade data.

Under the hood, the growth engine is running on specific cylinders: the consumer remains resilient (contributing over +2%) and net exports have swung from a drag to a massive tailwind (contributing just shy of +2%).

However, this strength masks underlying coolness in productive capital, as residential investment, nonresidential structures, and equipment spending are all currently acting as drags on growth. While the headline number is robust, the lack of broad-based economic investment is something worth keeping an eye on.

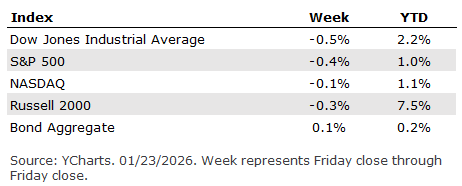

. . . U.S. financial markets navigated a volatile and politically charged week as investors balanced geopolitical tensions, corporate earnings, and shifting economic indicators. Equity performance was broadly flat to modestly lower, while Treasury yields fluctuated as investors weighed the implications of tariff threats, upcoming Federal Reserve decisions, and fresh economic data. Geopolitical stress dominated early-week volatility. Markets reacted sharply after President Trump threatened new tariffs against eight European trading partners, unless a deal on Greenland was reached, with proposed tariffs of 10% by February 1 and 25% by June. Investors weighed the implications on growth and inflation, leading to the largest one-day drop in the S&P 500 since similar tariff tensions in 2025. Uncharacteristically, assets that traditionally benefit during market stress (safe-haven assets - including U.S. Treasuries) also sold off (yields rose), reflecting the breadth of investor concern. Sentiment later stabilized after reports of a tentative security agreement over Greenland emerged, helping U.S. equities rebound late in the week. Corporate earnings, meanwhile, remained a central theme. Investor prepared for a heavy slate of earnings releases, particularly in AI-related companies, looking for confirmation of profitability trends. Broader earnings momentum also appears to be strengthening across multiple sectors, pointing toward potential broader market leadership in 2026. Economic data provided a more encouraging backdrop. Consumer sentiment climbed to 56.4 (indicating improving household outlook)2, while Manufacturing PMI rose to 51.9 and Services PMI held steady at 52.5, collectively signaling continued expansion and resilience in household and business activity.3 With the next FOMC meeting approaching, markets widely expected the Federal Reserve to maintain the current target range near term (3.50% - 3.75%), while still projecting rate cuts later in the year.4 The prior week clearly demonstrated that geopolitical noise can temporarily overshadow economic and corporate fundamentals. The broader narrative remains intact. Economic fundamentals continue to improve gradually, corporate earnings expectations are favorable, and monetary policy appears likely to ease over the course of 2026. While geopolitical risks may continue to spark volatility, the underlying market structure remains supported by growth, earnings, and increasingly stable inflation dynamics. The Federal Reserve Bank of Atlanta’s latest GDPNow model1 estimate for 4th quarter of 2025 surged to a striking 5.4%, a significant divergence from the Blue Chip consensus, which remains anchored near 1.0%. The model's estimate nearly doubled in early January, vaulting from 2.7% to the current high following the January 8 release of international trade data.

Under the hood, the growth engine is running on specific cylinders: the consumer remains resilient (contributing over +2%) and net exports have swung from a drag to a massive tailwind (contributing just shy of +2%).

However, this strength masks underlying coolness in productive capital, as residential investment, nonresidential structures, and equipment spending are all currently acting as drags on growth. While the headline number is robust, the lack of broad-based economic investment is something worth keeping an eye on.

[1] https://www.atlantafed.org/-/media/documents/cqer/researchcq/gdpnow/RealGDPTrackingSlides.pdf [2] Surveys of Consumers [3] S&P Global Flash US PMI [4] Fed Watch - CME Group

|