Five for Friday - January 23, 2026

Watching Yields, Japan in Focus, Small Caps, Productivity, and Shortages

1. Bonds

Political strategist James Carville once quipped, “I used to think that if there was reincarnation, I wanted to come back as the pope or a .400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody.” His point was that the bond market wields huge influence by acting as the mechanism that sets long-term interest rates (lower rates stimulate the economy…and are therefore politically desirable). If, however, investors deem a country’s policy path as fiscally unwise, they might sell that government’s bonds, thus increasing yields. This concept embodies the “bond vigilantism” of the ‘80s and ‘90s, though there are modern examples, as well (e.g., the UK’s 2022 budget crisis). Even this bull market, as robust as it’s been, has run into trouble when long-term yields have spiked. That’s what made this week’s action somewhat noteworthy. Despite recent anxiety over Fed independence and the U.S. fiscal trajectory, bond yields hadn’t risen much, which is a boon for stocks. This week the tone shifted, and yields broke out to multi-month highs. This bears watching (recall, higher yields had a moderating influence on tariffs in 2025). The extent to which Tuesday’s yield spike catalyzed the administration’s reversal on Greenland will likely never be known, but the bond market’s unofficial role as “fourth branch of government” seems intact for now.

2. Japan

Another example of bond vigilantism might be occurring with the massive spike (to multi-decade highs) in long-term Japanese government bond (JGB) yields this week amid fears that tax cuts pushed by Japan’s prime minister would strain already-stressed government finances (Japan has one of the highest debt-to-GDP ratios in the world). For investors, this matters because Japan's ultra-low / negative interest rates have long acted as a funding source for popular carry trades (investors can borrow cheaply in Japan to buy higher yielding assets elsewhere). A spike in Japan’s rates or a sharp currency move can force investors to unwind these positions, sparking a waterfall of selling across asset classes and around the globe. This was the case in August 2024, when an unexpected Bank of Japan rate hike sent the S&P 500 down more than 6% in three days (before it recovered nearly as quickly). It doesn’t change the fundamentals of underlying assets, but it does remind us how interconnected (and butterfly effect-y) today’s markets can be.

3. Small

Another tidbit from Tuesday’s selloff was that small caps outperformed large caps meaningful which is rare on a big risk-off day. In the last decade, there have been 4 trading sessions in which the S&P 500 fell 2% or more while the small cap Russell 2000 outperformed as much as it did Tuesday. This hot start from small caps could be a good sign. In the last two decades, there were 9 times that small caps outpaced large caps through this point in January and in all of those years the stock market finished the year higher…with an average return of 22%. Small caps are not immune to geopolitical turmoil (even tiny firms have global supply chains these days), but they do more business at home than abroad. If small cap performance is an indicator of confidence in the U.S. economy, this strong start is a good sign for growth.

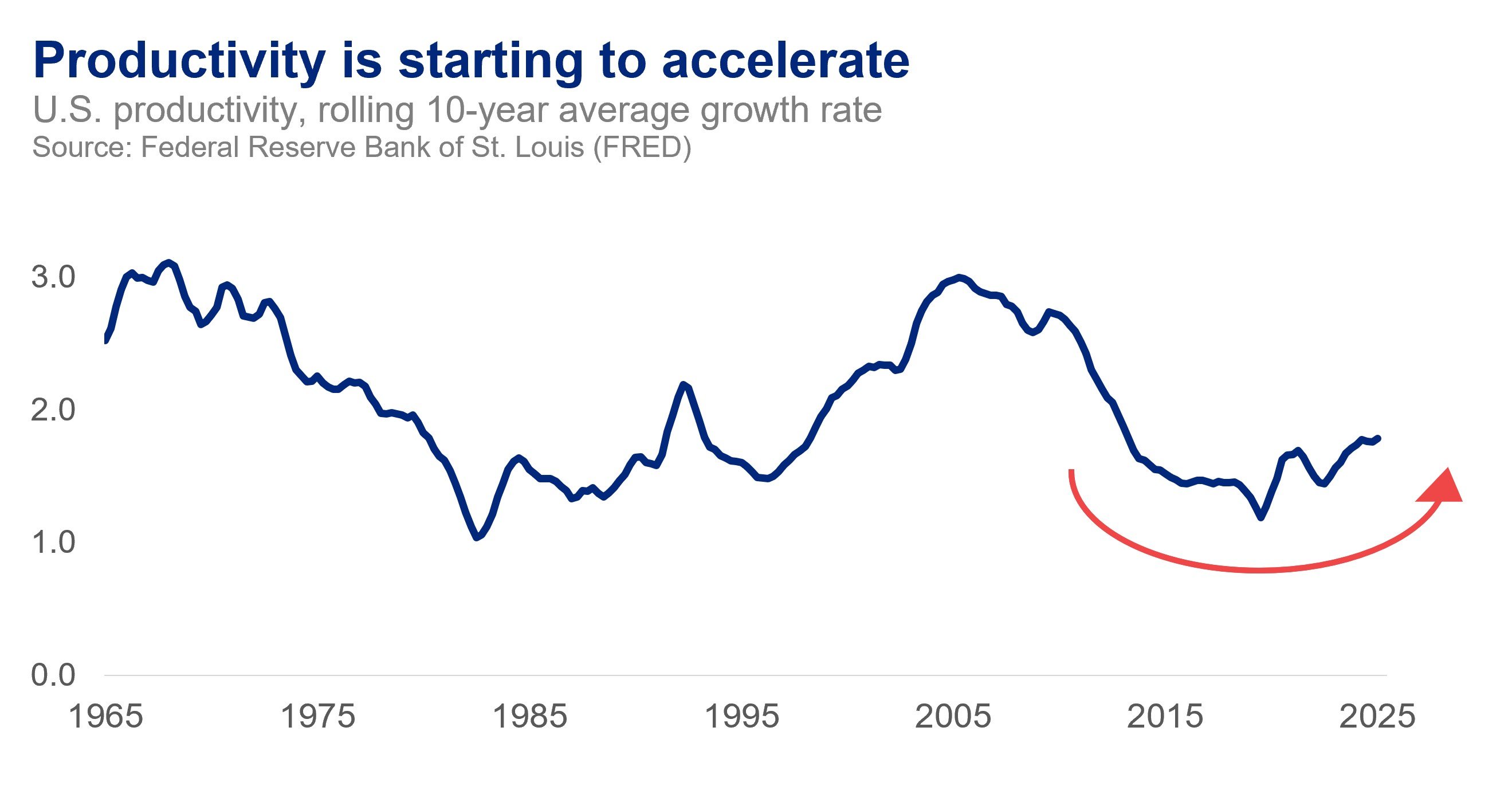

4. Productivity

is any economy’s secret sauce. The ability to produce more stuff with the same or fewer inputs—a more efficient labor market—leads to growth (sans inflation), more profitable companies, and a more sustainable debt backdrop. The U.S. already dominates global productivity statistics, but growth is accelerating.

5. Cool paper alert

Some researchers created a news-based index tracking U.S. shortages of industrial goods, energy, food and labor in the U.S. since 1900—a worthwhile effort as major shortages are associated with high inflation and weaker growth. Currently, the overall index is near post-Covid lows and well below periods of high inflation like the 1970s, but labor shortages are near post-WWII highs. This is a major economic theme for the coming years.

Disclosures

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Market and economic statistics, unless otherwise cited, are from data provider FactSet.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should not consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For investment advice specific to your situation, or for additional information, please contact your Baird Financial Advisor and/or your tax or legal advisor.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Copyright 2025 Robert W. Baird & Co. Incorporated.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.